DSV Global Market update – AUGUST 2024

Dear customers,

Please find attached the market update for August 2024 for Air & Sea.

DSV Israel

DSV GLOBAL UPDATE – Presentation

LOCAL UPDATE

Ocean

- The red sea crisis is still influencing the traffic from the Fareast to Israel and the global market as well.

- Most of the shipping lines have decided, to stop all voyages through the Suez Canal for the time being, and to have their vessels operate via the Cape of Good Hope.

- Other options are shipping by ocean from the Fareast to Bahrain or Jebel Ali ports, trucking to Sheikh Hussain, clearing from customs at the cross border, trucking the shipments to final destinations in IL.

- The situation causes longer transit time, lack of capacity, and shipments switched from Ocean to Air to meet the lead time.

- India – due to the congestion at Indian ports, Zim postponed bookings into Israel until the end of August 2024, more demand on Air transportation which effecting capacity and rates increase.

Airfreight

- The airports in Israel are operating as usual, Israeli & most of the international airlines are operating as usual.

- Some of the International airlines have suspended their flights into/from Israel in August due to the Iranian threat , and are gradually starting to resume operations

- AIR CANADA & Air India – The flights are temporary suspended expected to return in October 2024.

- There may be changes due to the situation, we will continue to monitor and update accordingly few international airlines are postponing resuming their flights to/from Israel since the 7th Oct 2023 due to the war.

Political crisis with Turkey

- The political crisis with Turkey gives its signals in the supply chain especially in ocean/air traffic to Israel, direct sailings from Turkey are possible for Palestinian customers only and without the involvement of an Israeli forwarder.

- DSV Israel is working to find alternative solutions for its customers,

Please contact our service and sales representatives for additional information and import solutions.

GLOBAL

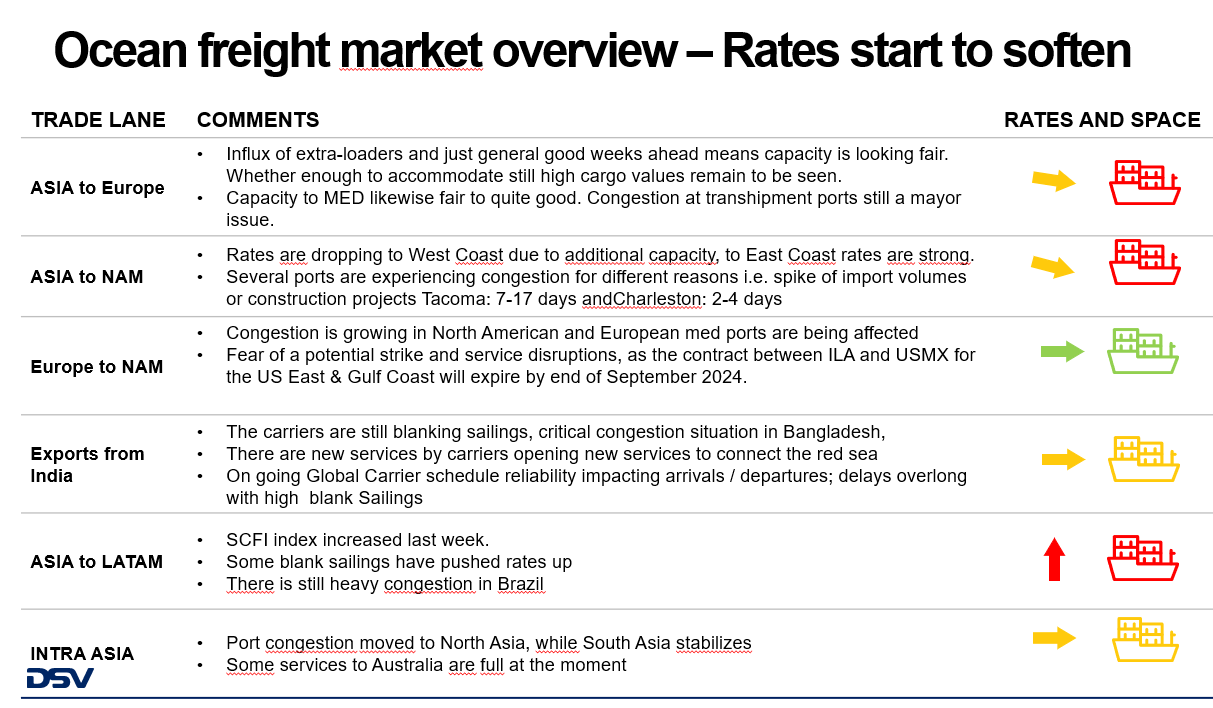

Please find attached a new monthly market update. Port congestion is still an issue, and it is growing on main China ports and destination ports in North America and Europe. We reached the peak on SCFI in the middle of July and rates are started to slowly soften. Airfreight rates are very strong out of Asia given that this time of the year is the slow season.

Together with the market update there is a presentation of FUEL-EU, in addition to the fuel consumption and related GHG emissions, the FuelEU Maritime directive, also follows a “zero-emission port stay” objective, means passenger and cargo ships are required to connect to onshore power supply at major EU ports from 2030 and all EU ports by 2035. This will also add pressure to port owners to invest in such onshore power supply infrastructure over the upcoming years. In consequence carriers will face higher costs during berthing time or handling charges per TEU with the market. The scope of this initiative is on EU countries, similar to the implementation of ETS charges.

OCEAN: During last month, SCFI had a decrease of -11,5% which seems that we have reached the peak of rates. We are in the middle of peak season, and we are seeing record volumes being imported for the first time since April 2024, driven by Asia to West Coast with a -4%. For Asia to Europe and Asia to US East Coast are still strong. There are some expectations that rates will reach a plateau when we are now in the middle of the peak season. We have another record month in terms of volume, during July the US imported 2,5 Million TEU, these numbers where only seen during the peak of cargo during COVID.

AIR: Worldwide rates have risen progressively despite of being “slow season”, there is similar capacity available and growth in volumes from Asia. Asia Pacific to the USA was among the key lanes driving up overall average prices.

DSV is Launching a new product called “Movie Star” Singapore – Los Angeles

Due to very high demand in Asia, more than in America and Europe (airfreight), airlines are expected to reallocate capacity from America and Europe to Asia to capitalize on higher profits in Asia.

This means, starting from September, the capacity on transatlantic routes (Europe-USA) will decrease, leading to a significant increase in prices.

- DSV is Launching a new product called “Movie Star” – operating a weekly charter B777-200Freighter service starting September 3rd on the Singapore–Los Angeles route, i.e., Far East to USA.

- DSV is operating twice a week charter services “Blue Wings” from Alabama, USA, to Luxembourg, i.e., USA to Europe

Tenders: We are still on slow season, now that ocean rates start to soften, we are working on preparation for a tender peak season by the end of September beginning of October. We are seeing very different markets both in Ocean and Airfreight, where pricing from Europe and North America are stable and is good to negotiate long term agreement while exports from Asia are now very volatile and the best way is to negotiate short term deals to make sure that cargo is moved.

General Update

- Global economy grew 3.2% in 2023 and is forecast to grow at the same pace during both 2024 and 2025

- Retail sales in both the EU and US have remained mostly static despite improving consumer confidence.

- The developing trade disputes between the EU & US and China could impact global trade.

- US Gains Ground in Global Chip Market: US share of worldwide fab capacity is projected to reach 14% by 2032 up from 10% today. It would have slid to 8& without the chips Act.

Ocean freight highlights:

- Port congestion is peaking up again at 2,4m TEU (7,9% of fleet)

- Ningbo port (China) explosion adds pressure to trans-Pacific container trade.

- Bangladesh port congestion continues to build up over the past weeks.

- We have the largest gap ever on Spot vs Long-term rates since the Pandemic – Carriers are applying PSS.

- Another record-breaking month for container shipping demand from China to North America and North Europe,

- July’s U.S. container import volumes rose by 11.2% from June 2024, reaching 2,556,180 twenty-foot equivalent units (TEUs).

- New data from the US Census Bureau, detailing both sales and inventory changes in the US up until the end of April 2024, shows absolutely no signs of a sudden surge in container demand prior to the sharp rise in container spot rates in early May 2024

- Carrier “on time” reliability up in June to 54.4%, no recovery since the Red Sea attacks

Airfreight highlights;

- It is expected a strong H2-24 for Airfreight between Asia to Europe and North America

- Global international air cargo capacity up by +7% (vs 2019) between July 8th and August 4th in 2024

- Global international air cargo capacity growth remains stable in the last four weeks.

- Integrator driven air cargo capacity growth from Asia shows a contrast between the North and South of the region.

- Global international air cargo capacity shows resilience after the major global IT failure.

- Global tonnages (+9%) and rates (+12%) continue to show strong YoY improvements.

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Time Critical Services

When it’s urgent and you need something delivered fast

Special project transport

Out of gauge and anything non-standard

Rail freight

The greener alternative from China to Europe and within Europe and North America

Road transport

Local, long distance, national or international

Sea freight

When cost matters and time is not an issue

Air freight

When time and speed matter most

Air freight

When time and speed matter most

Sea freight

When cost matters and time is not an issue

Road transport

Local, long distance, national or international

Rail freight

The greener alternative from China to Europe and within Europe and North America

Special project transport

Out of gauge and anything non-standard

Time Critical Services

When it’s urgent and you need something delivered fast

הפקת דוחות פליטות פחמן

יעוץ תכנון וניהול פרויקטים רחבי היקף בארץ ובחו”ל

Latest news

Flash update – 26/03/2026

Flash update – 24/03/2026

Ocean carriers – Breakdown of fuel and war-related surcharges

Flash update – 23/03/2026

Flash update – 22/03/2026

Flash update – 22/03/2026

#2 Flash update – 19/03/2026

Flash update – 19/03/2026

Flash update – 18/03/2026

Flash update – 17/03/2026

Flash update – 16/03/2026