DSV Global Market update – January 2025

Dear Customers,

Please find attached a new monthly market update January 2024.

DSV Israel

LOCAL UPDATE

Air Freight

- Due to the security situation in the region, several airlines are extending the suspension of flights to and from Israel. Some are expected to gradually resume operations.

- This situation creates significant pressure on Israeli airlines and the international airlines operating to and from Israel.

- Lufthansa Group (including SwissAir, Austrian Airlines, and Brussels Airlines) announced the resumption of operations to and from Israel starting February 1.

- Air France – Expected to resume operations by January 30.

- ITA Airways – Expected to resume operations by February 1.

- Air Baltic – Expected to resume operations by March 25.

- Reduced capacity is causing extended transit times.

Ocean Freight

- As of now, there are no changes in ocean freight operations. Ports in Israel are functioning normally.

- The crisis in the Red Sea is impacting trade between the Far East and Israel.

- Shipping lines sailing to and from Israel are avoiding the Red Sea and rerouting via Africa’s Cape of Good Hope.

- This situation is extending transit times by approximately 20 days, reducing container capacity, and shifting some shipments from ocean to air freight to shorten delivery times.

Land Border Crossings

- The Allenby Border Terminal cargo section is operating partially, following Israeli customs guidelines.

- Other border crossings are functioning as usual but experiencing congestion due to the diversion of shipments from Allenby to other terminals.

Political Crisis with Turkey

- The political crisis with Turkey continues to impact the supply chain, particularly maritime transportation to Israel.

- Direct sailings from Turkey are permitted only under restrictions for Palestinian clients, with no involvement of Israeli forwarders.

- DSV Israel is actively working to find alternative solutions for its clients.

Please contact our teams for additional information and tailored solutions.

Global

General Update

2025 has begun on a positive note. The looming strike on the US East Coast, which was threatening to create supply chain turmoil yet again, has been cancelled. The union and the employers at the container terminals have come to an agreement for a new master contract after months of disagreement, especially regarding the topic of automation. Presently, the details of this new contract have not been made public, and hence the long-term impact and costs of the agreement are not known. However, irrespective of this, it is certainly positive news with which to begin 2025.

We still need have following key items pending:

Donald Trump inauguration day, as president of USA and potential announcement of new imposing 25% tariffs on Canada and Mexico and additional 10% tariffs on China

Feb 1st : Starting of the new shipping alliances, cooperations & services: MSC, Gemini Cooperation, Premium Alliance and THE alliance.

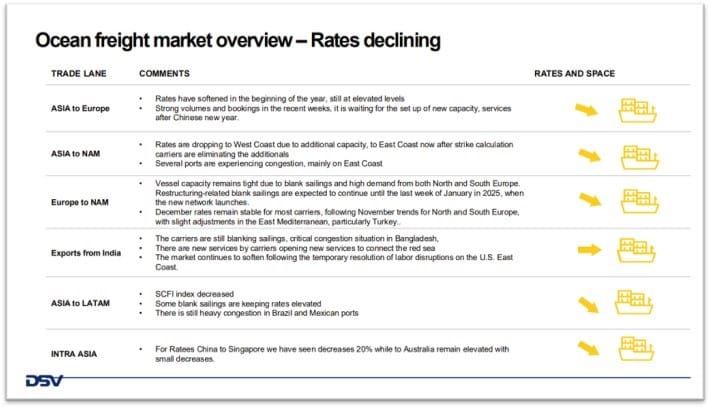

OCEAN: Rates have been correcting during the beginning of the year after rate increases implementation and waiting for a potential correction after Chinese New Year; SCFI during last month decreased -3.9%, driven by a normalization of North American destinations. There is heavy port congestion at the moment at Shanghai/Ningbo as well as Rotterdam and some east coast ports..

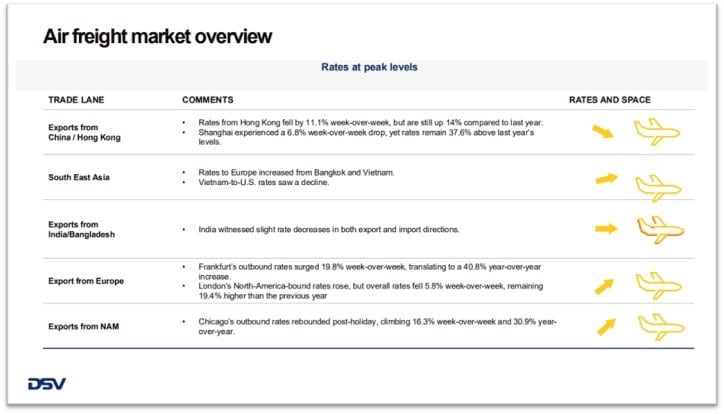

AIR: The year has started soft in terms of volumes and rates, and we are expecting the shipment rush before Chinese New Year. E-Commerce volumes from Asia have stopped (cargo is mainly shipped now on ocean), and we expect the start of low seasonality in February..

Tenders: We are on tender peak season; a large number of tenders is being launched, and at the moment there is a big unknown if long-term rates will converge with higher spot rates. The workload is for both Air and Ocean modes at the moment, and we expect final awards to come by the end of February and March.

For the DSV teams in China, wishing you all a Happy Chinese New Year and a prosperous Year of the Dragon!

General Update

- Chinese trade surplus soars to USD 1 Trillion Ahead of Trump Return

- US trade restrictions are set to reshape a foundational supply chain in the technology sector

- U.S Economy Surprised Again in 2024, The job gains in December were much higher than the roughly 160,000 analysts had expected: Employers added 256,000 jobs and the unemployment rate dropped from 4.2% in November to 4.1%

- European Central Bank Must Find ‘Middle Path’ on Rate Cuts, The European Central Bank will continue to lower its key interest rate, but must do so at a pace that ensures inflation continues to cool.

- German economy shrinks for second year in a row, Europe’s largest economy contracted by 0.2% on 2024, after shrinking by 0.3 % in 2023

- Tougher US sanctions to curb Russian oil supply to China and India, The U.S. Treasury imposed sanctions on Russian oil producers Gazprom Neft (SIBN.MM), as well as 183 vessels that have shipped Russian oil, targeting the revenues Moscow has used to fund its war with Ukraine

Ocean freight highlights

- US East Coast: With Port Strike Averted, Dockworkers Draw New Curbs on Automation

- Ocean container market in 2024: As per CTS there is strong growth on major trades, and the total volume loaded from January to November 2024 is up 6.0%. For global container shipping, this is a very high growth rate and indicates a strong market.

- China’s Chancay Megaport in Peru Opens

- China’s biggest shipping line Cosco added to US military blacklist

- 2025 is the year of the first major alliance-free carrier: MSC

- Carrier on time Performance at 54,8%

- Strong December U.S. Container Imports Close 2024 but Potential Challenges Loom for 2025, This year also marks the third-highest annual volume on record just 3% behing the pandemic record.

Airfreight highlights

- Macro disruptions for 2025: Anticipation of trade tariffs, lack of new freighter, red sea impact, mandatory sustainability charges.

- At +9%, Q4 2024 is anticipated to mark the 4th consecutive quarter of year-over-year growth in global air trade volumes.

- 2024 global air trade is expected to record +5.7% growth while showing notable contrasts between major trade lanes.

- Transatlantic westbound market had large increases during last two months of 2024.

Asia Outbound will continue to be the most constrained market with high volatility in the rates.

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Special project transport

Out of gauge and anything non-standard

Time Critical Services

When it’s urgent and you need something delivered fast

Special project transport

Out of gauge and anything non-standard

Rail freight

The greener alternative from China to Europe and within Europe and North America

Road transport

Local, long distance, national or international

Sea freight

When cost matters and time is not an issue

Air freight

When time and speed matter most

Air freight

When time and speed matter most

Sea freight

When cost matters and time is not an issue

Road transport

Local, long distance, national or international

Rail freight

The greener alternative from China to Europe and within Europe and North America

Special project transport

Out of gauge and anything non-standard

Time Critical Services

When it’s urgent and you need something delivered fast

הפקת דוחות פליטות פחמן

יעוץ תכנון וניהול פרויקטים רחבי היקף בארץ ובחו”ל

Latest news

DSV IL – Flash update 03/03/2026

DSV IL – Flash update 02/03/2026

DSV Global Market Update – June 2025

DSV IL – Flash update 13.06.2025

DSV IL – Flash update 09.06.2025

DSV IL – Flash update 03.06.2025

DSV IL – Flash update 22.05.2025

DSV IL – Flash update 5.02.2025